How auto parts tariffs could raise car insurance premiums in 2025

Trending News

Audio By Carbonatix

8:30 AM on Thursday, September 4

By Evan Ullman for CheapInsurance.com, Stacker

How auto parts tariffs could raise car insurance premiums in 2025

Car insurance costs are already climbing, and newly proposed tariffs on imported auto parts could push rates even higher.

It’s a straight line: The U.S. has imposed a 25% tariff on assembled vehicles and a 25% tariff on certain auto parts. Mitchell analysts expect these parts tariffs to lift collision repair costs, especially for electronics and ADAS components, which in turn can pressure premiums.

CheapInsurance.com breaks down which states and drivers could be hit hardest, especially in high-cost areas like Florida and Louisiana, import-heavy states, and among lower-income households.

How the 25% auto parts tariff could hit your premiums

Experts expect vehicle repairs to become more expensive after the 25% tariff on imported auto parts, effective May 3, 2025, and insurers will likely pass those costs to drivers. Analysts at Mitchell International say the price hikes could start hitting consumers by mid-to-late summer.

The chain reaction is simple: Higher part costs lead to more expensive repairs, bigger insurance payouts, and finally, premium increases. The National Law Review notes that tariff-impacted parts include engines, transmissions, electrical systems, and ADAS sensors, notes, some of the priciest to replace.

Key numbers

- There could be an additional $20-$50 per repair involving tariffed parts, per MotorBiscuit reporting.

- Bureau of Labor Statistics data show auto insurance premiums rose 11.3% year over year in 2024.

- More than 30% of auto parts are imported from Mexico and Canada, according to a GlobalData consumer survey.

The White House notes that parts from Canada and Mexico are exempt for now under the United States-Mexico-Canada Agreement, but that could change once a collection system is finalized.

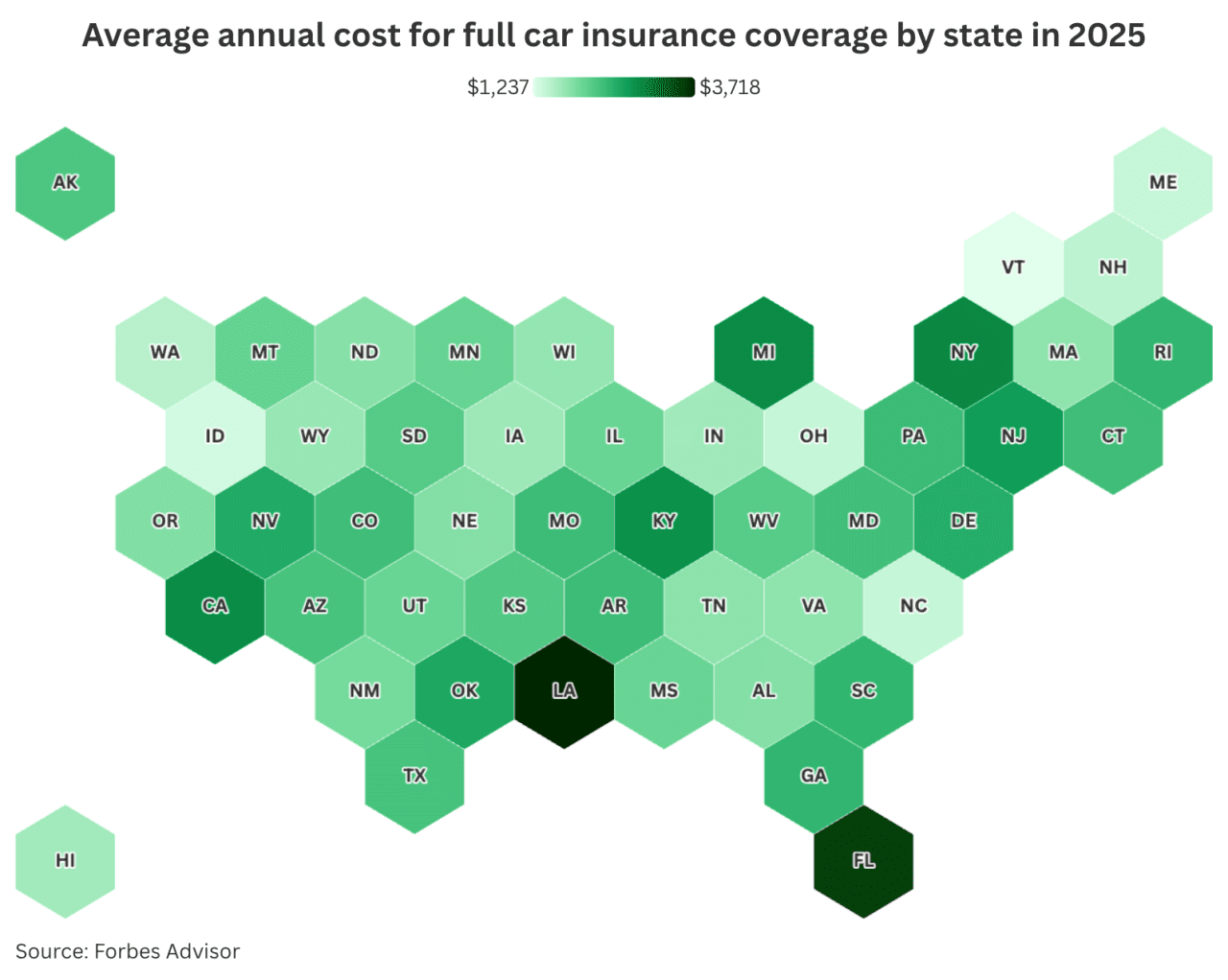

States most vulnerable to tariff-driven premium increases

Tariffs on auto parts won’t hit all states equally — some are far more exposed due to high premiums or heavy reliance on imports.

High-premium states take a bigger hit

According to World Population Review, places like Nevada ($3,439), Florida ($3,267-$3,950), and Louisiana ($2,989-$3,626) already had some of the highest rates in the country as of March 2024. Because tariff-related hikes are percentage-based, drivers here could end up paying more per vehicle.

Import-heavy states are also at risk

Michigan, Texas, and California, all key auto manufacturing and assembly players, depend on foreign parts and face similar exposure.

Already-rising states could get hit twice

The map below shows where these risks are concentrated, highlighting which states are likely to feel the biggest impact.

Demographic groups most affected

Tariff-driven premium hikes won’t hit everyone the same. Lower-income families, multicar households, and rural drivers are likely to feel the biggest pinch.

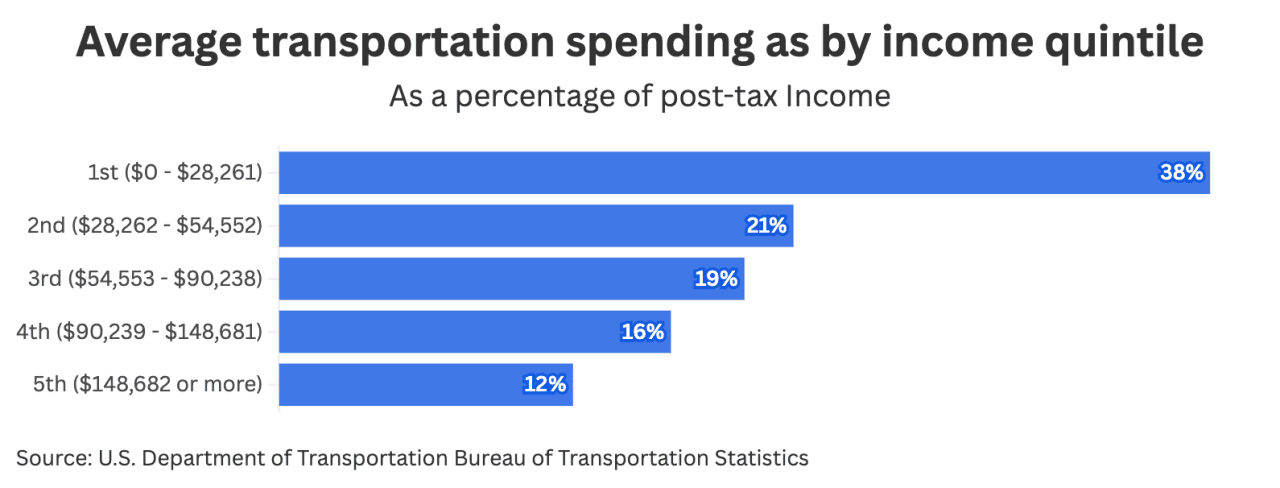

Lower-income households

According to the Peterson Institute for International Economics, tariffs hit households earning under $50,000 the hardest, and drivers earning under $50,000 already spend a big chunk of their income on transportation. As the chart shows, the bottom income group spends 38% of their post-tax income on it, over three times more than the wealthiest.

Multivehicle families

Middle-income families with multiple cars will see the impact multiply. According to the Bureau of Transportation Statistics, as of 2023, over 35% of households owned two vehicles, and over 20% of households owned three or more cars.

Urban and rural drivers

Urban drivers face higher base premiums, so even a small percentage increase means a bigger dollar jump. In rural areas, limited repair shops and fewer part suppliers could push both repair and insurance costs even higher.

Industry expert projections and modeling

Experts across insurance, economics, and government agree: Tariffs on imported auto parts could drive major cost increases for consumers.

Insurance industry outlook

University of South Carolina’s Robert Hartwig, director of the university’s Risk and Uncertainty Center and clinical associate professor of finance, projects $35-$120 in premium hikes per vehicle, depending on the car and repair needs.

Economic research perspectives

Swiss Re predicts the deceleration of auto insurance prices as claim inflation slows down. However, LexisNexis reports “nuclear” levels of auto insurance shopping near the end of 2024 and elevated levels in Q1 of 2025.

Government and academic data

National Association of Insurance Commissioners data shows the average premium hit $1,258 in 2022, up 5.75% from 2021. According to the U.S. Treasury, auto insurance in 2023 made up 35.8% of the entire property and casualty market, meaning even small pricing shifts carry big ripple effects.

Regional variations and state-specific factors

Tariff-driven premium hikes won’t roll out evenly. State-level regulation, geography, insurance market differences, and more will shape how hard drivers are hit.

Regulatory limits

States like California and New York require approval before insurers can raise rates. That may delay increases, but it won’t block them entirely if repair costs spike.

Geographic risk

States like Florida and Louisiana already face high premiums due to hurricanes, flooding, and theft. Add rising repair costs to the mix, and premiums there could climb even faster.

Market dynamics

In states with fewer insurers or limited competition, companies may raise rates more aggressively without losing customers.

Infrastructure strain

Places with fewer repair shops or heavier reliance on imported parts may see slower claims processing and sharper cost hikes as supply chain pressure builds.

Consumer response and behavioral changes

As insurance costs rise, consumers aren’t just absorbing the hit. They’re changing how they spend and insure, by:

- Shopping for better rates.

- Tweaking coverage. Putting off car purchases.

- Cutting other expenses.

These shifts show how federal policy changes are directly reshaping day-to-day household decisions.

What drivers can expect and how to prepare

Tariff-driven price hikes are set to reshape the auto insurance landscape, hitting hardest in high-premium, import-reliant states like Nevada, Florida, and California. Lower-income and multicar households will likely feel the strain most.

Drivers can expect rate increases starting mid-2025, with full effects playing out into 2026. These changes highlight the need for transparency and proactive steps like shopping around and adjusting coverage.

Looking ahead, supply chain improvements and possible tariff rollbacks could ease some pressure. But for now, staying financially sharp is key to navigating what’s shaping up to be another costly chapter for American drivers.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.